With initial claims increasing, the BLS will find it more difficult to report fake unemployment rates. My model suggests confidence will collapse when the rate hits 4.2-4.2 percent.

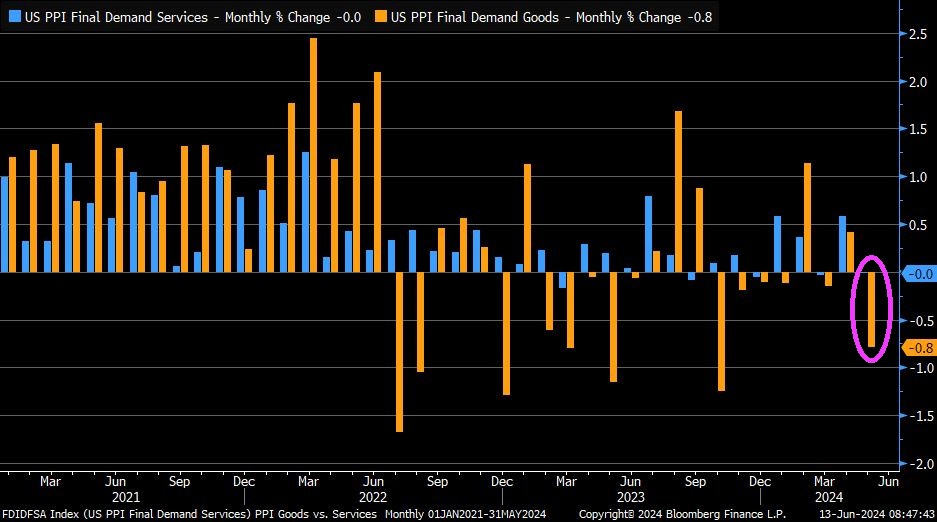

While consumers expect more inflation, the PPI Final Demand Index declined on weak demand for domestic goods and services, suggesting that inflation may cool off with the economy once the recession begins.

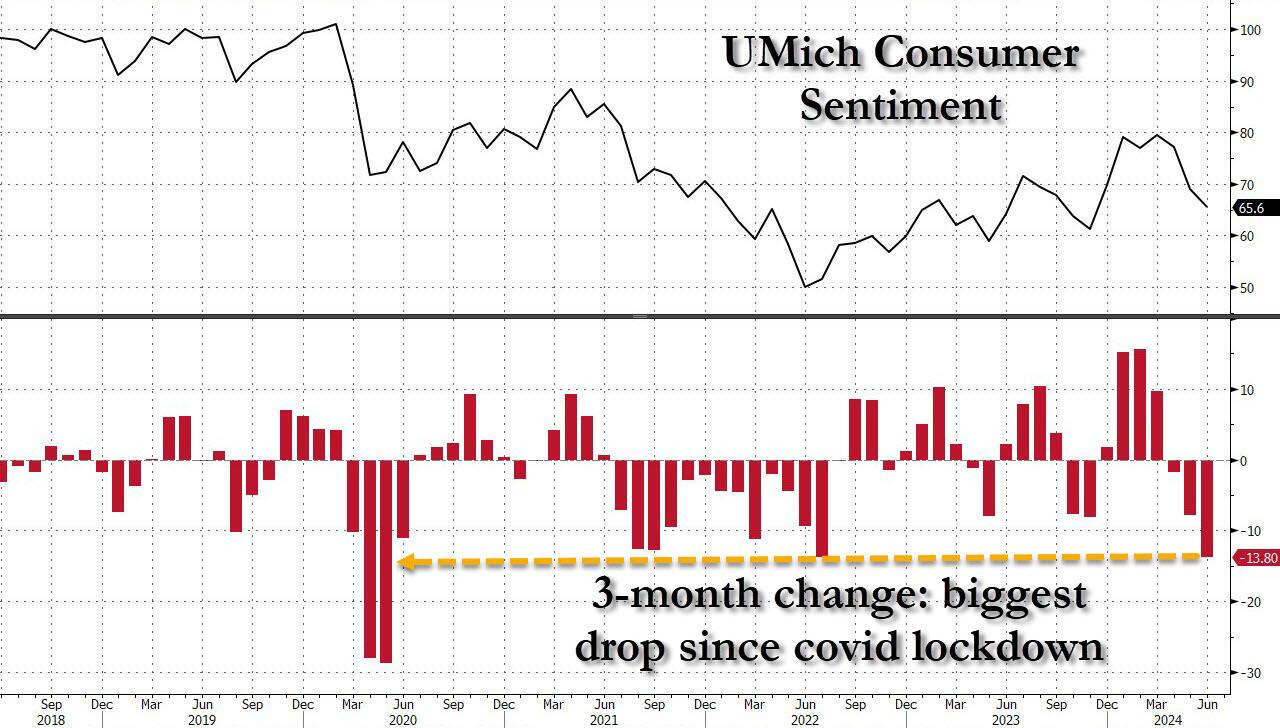

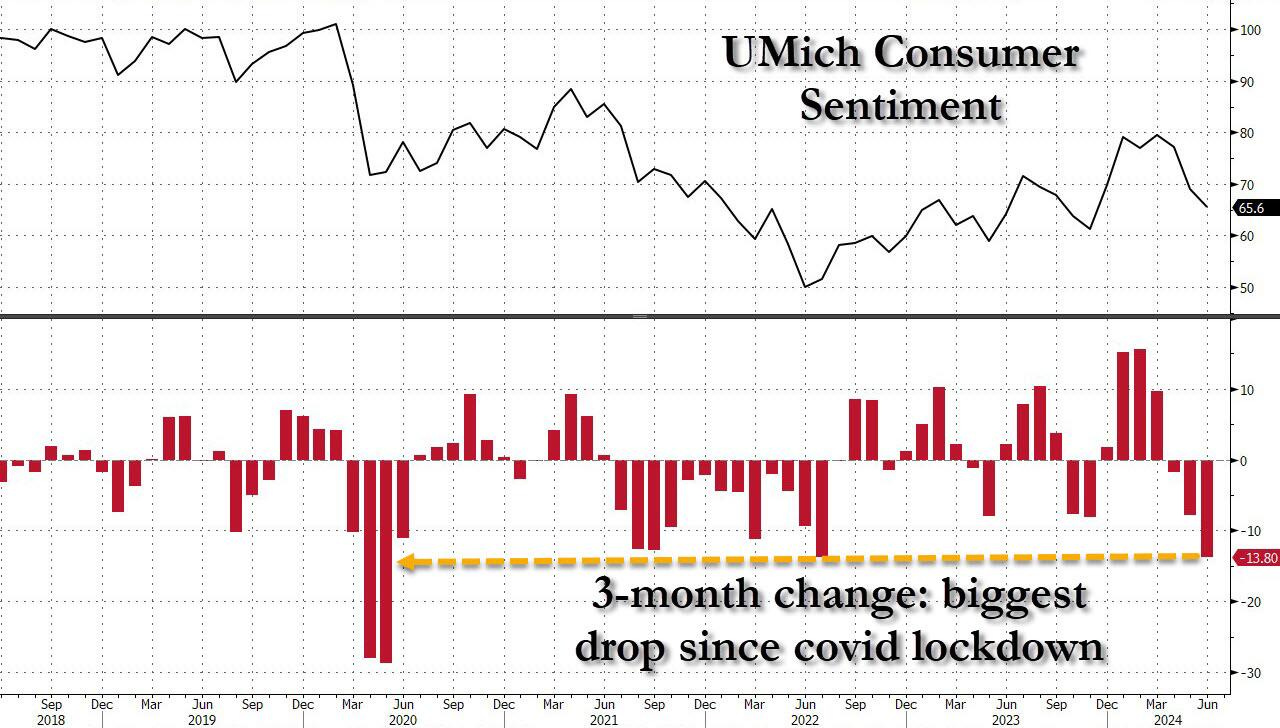

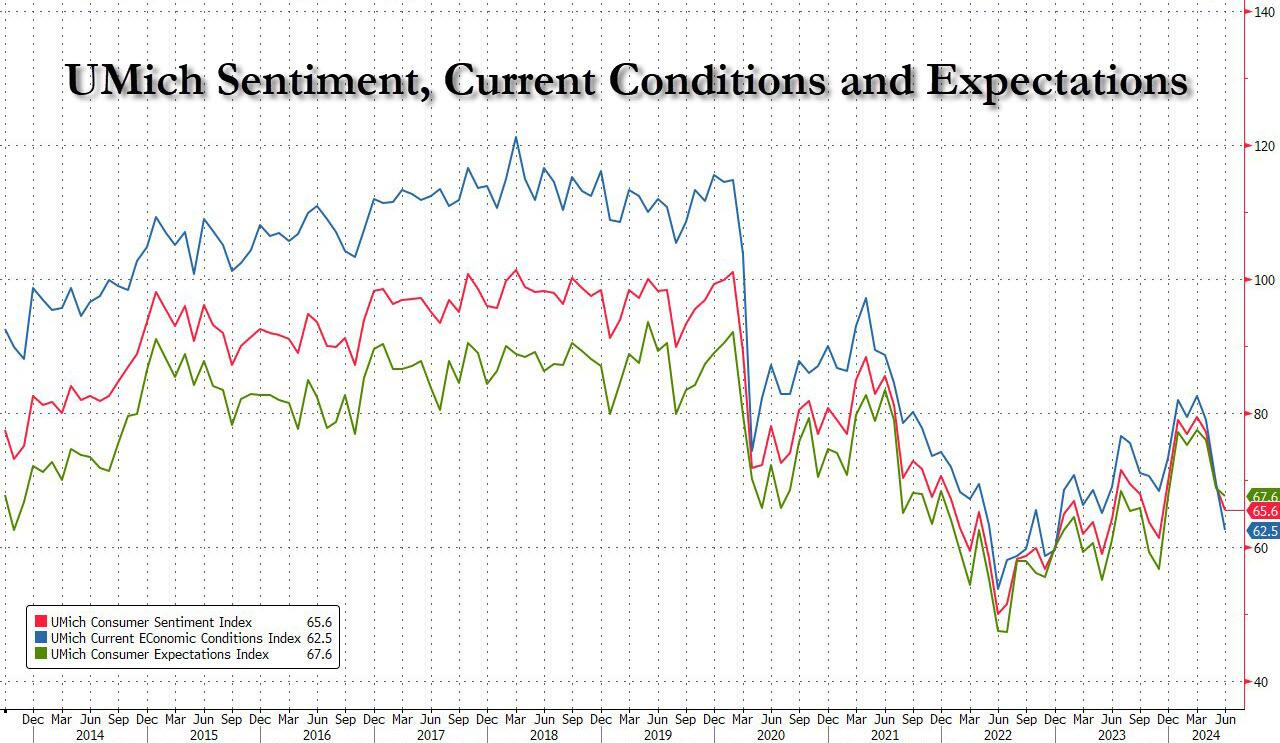

One month after the May Consumer Sentiment printed at a record 7-sigma miss to expectations, consumer sentiment once again “unexpectedly” slumped, this time from an upward revised 68.8 to 67.6, the lowest print since last November, and the biggest 3-month drop in sentiment (-13.8 points) going back to the covid lockdowns.

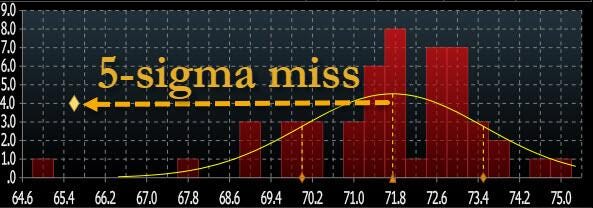

… which was not only a 5-sigma miss to the median estimate (an improvement from last month’s 7-sigma)…

… but also the biggest miss of 2024.

The collapse in sentiment was broad based, and hammered both current conditions – which plunged from 69.6 to 62.5, the lowest since 2022 and badly missing estimates of 72.2 – and also expectations, which dropped from 68.8 to 67.6 (and also far below the 72.0 estimate).

The decline in sentiment coincides with signs that the labor market, which has driven consumer spending over the last year, is also falling apart. The unemployment rate rose to 4% last month, the highest in more than two years, while jobless claims unexpectedly soared following a firing frenzy out of California.

“While lower-income families have, as a group, seen notable wage gains in a strong labor market, their budgets remain tight amid continued high prices even as inflation has slowed,” Joanne Hsu, director of the survey, said in a statement.

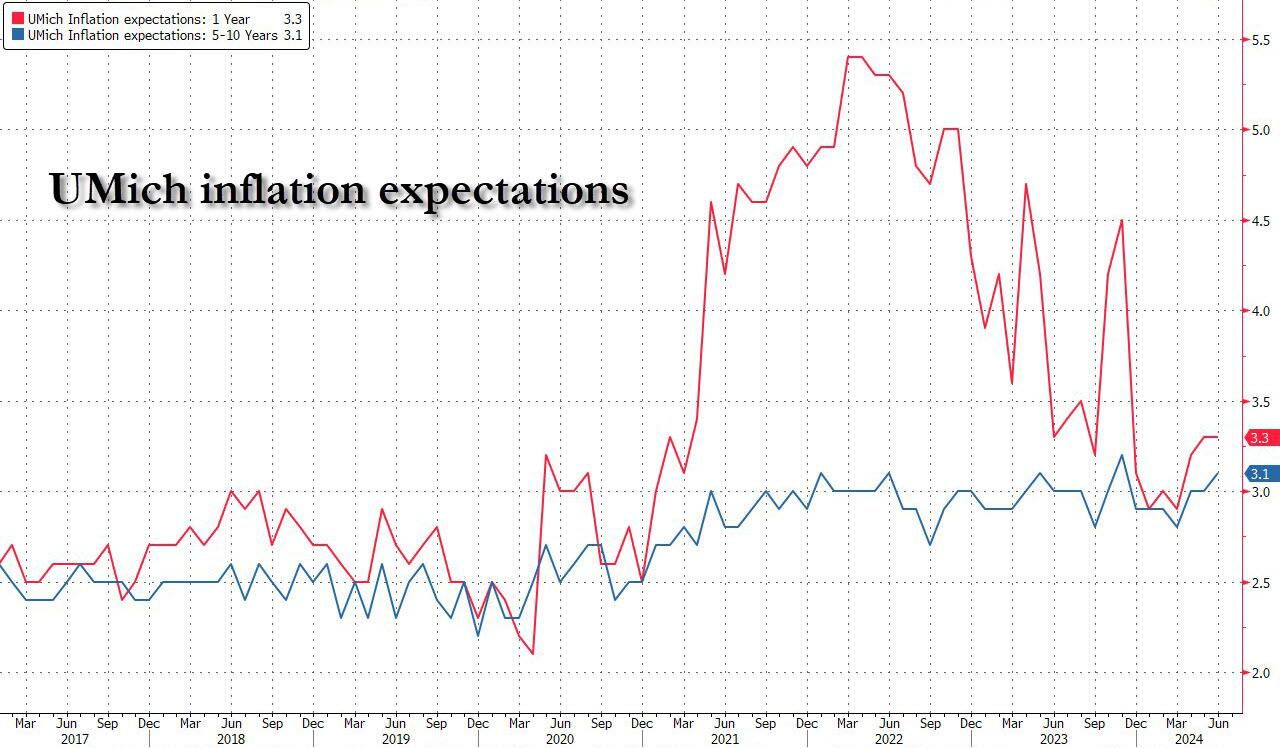

But wait there’s more, because if that was the “stag” part of the report, the UMich report also confirmed that the “flation” isn’t far behind, as the inflation outlook continued its recent deterioration, to wit: 1 Year inflation expectations remained unchanged at 3.3%, beating estimates of a drop back 3.2%, while 5-10 Year inflation expectations rose from 3.0% to 3.1%, the highest since November.

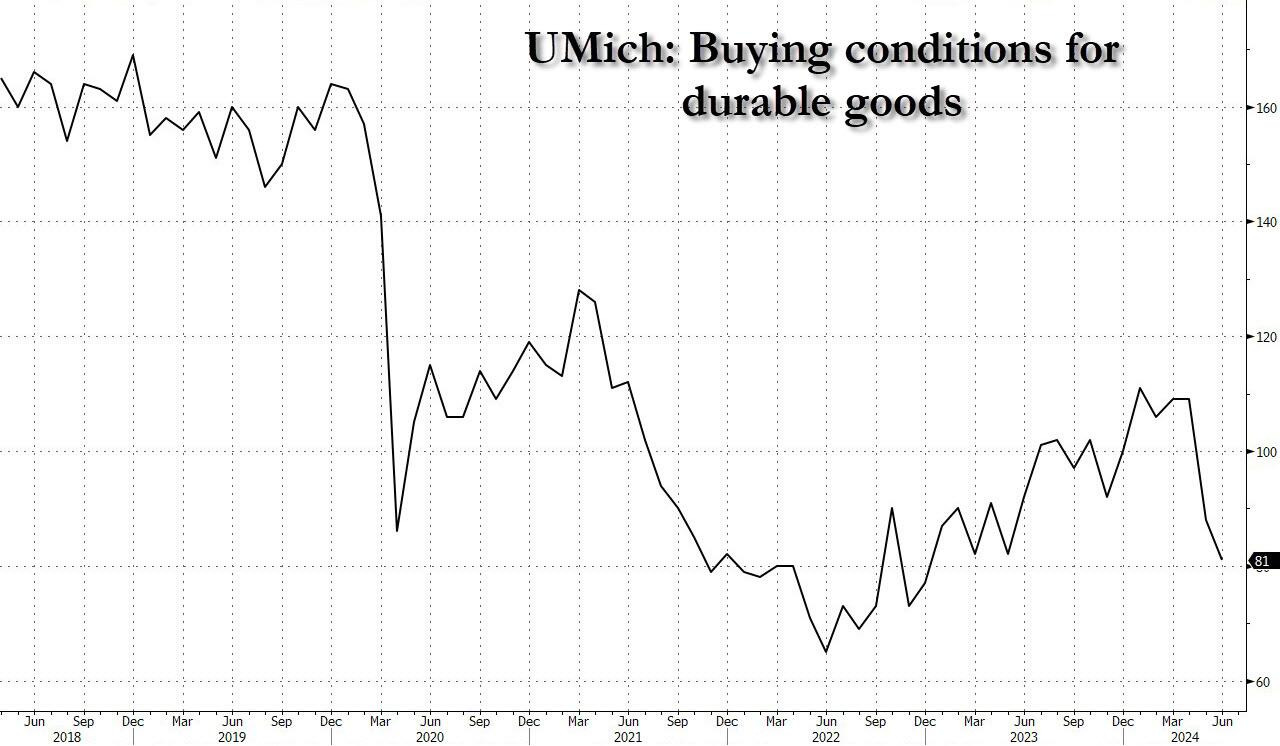

If that wasn’t enough, the slide in sentiment suggests restrained consumer demand in coming months. The university’s measure of buying conditions for durable goods decreased to the lowest level since December 2022, a glowing testament to just how tapped out the US consumer truly is.

In short: the verdict for Bidenomics is in, and it’s a complete disaster, as for Powell’s recent laughable comment that he can’t see the “stag” nor the “flation”… well, Fed chair, they just bit you on the ass.

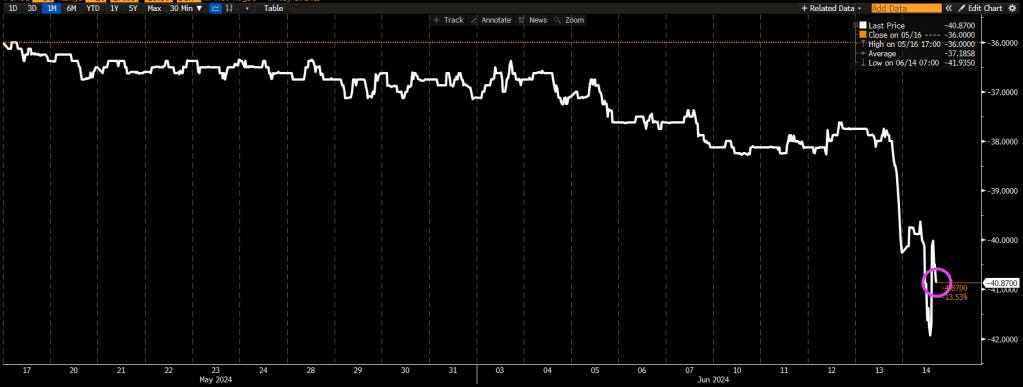

On top of a poor consumer sentiment report, the PPI Final Demand index was down … again.

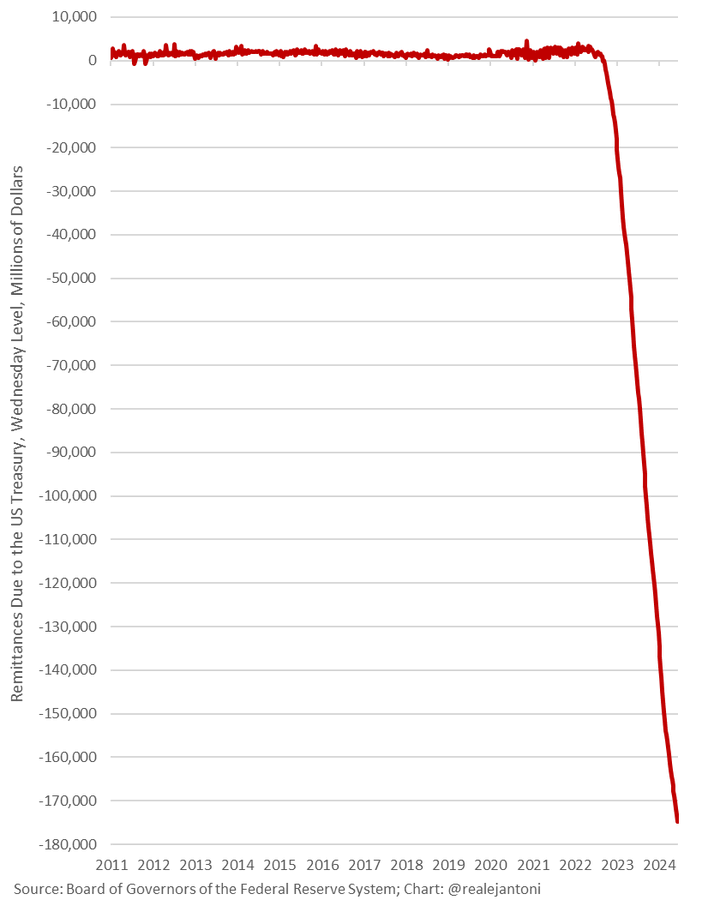

Here is more information on the Fed’s remittances to the Treasury from MS Copilot GPT-4:

The Federal Reserve's remittances to the U.S. Treasury represent the transfer of the Federal Reserve's net earnings to the Treasury. Here’s a detailed explanation:

What Are Fed Remittances?

Net Earnings: The Federal Reserve generates income primarily from interest on U.S. government securities it holds in its portfolio. Other sources include interest on foreign currency investments, fees from services provided to financial institutions, and interest on loans to depository institutions.

Expenses and Dividends: From this income, the Federal Reserve deducts its operating expenses, the cost of producing and issuing currency, and dividends paid to member banks, which are required shareholders in the regional Federal Reserve Banks.

Surplus and Remittances: The remaining net earnings (surplus) are then remitted to the U.S. Treasury. These remittances are transferred weekly and reported annually in the Federal Reserve's financial statements.

Importance of Fed Remittances

Revenue for the Government: These remittances provide a source of revenue for the federal government, reducing the need for borrowing and helping to fund government operations.

Monetary Policy and Fiscal Policy Interaction: The size and frequency of remittances can reflect the broader economic environment and the Federal Reserve’s monetary policy actions. For example, higher remittances often occur when the Federal Reserve's balance sheet is larger due to quantitative easing policies.

Transparency and Accountability: Regular remittances and detailed financial reporting enhance the transparency and accountability of the Federal Reserve’s operations.

Recent Trends

Quantitative Easing: During periods of quantitative easing, the Federal Reserve's holdings of government securities increase, potentially leading to higher earnings and, subsequently, higher remittances to the Treasury.

Interest Rate Changes: Changes in interest rates can affect the Federal Reserve's earnings. For example, when interest rates are low, the earnings from the Federal Reserve's portfolio might be lower, impacting the size of the remittances.

Annual Reporting

Financial Statements: The Federal Reserve publishes annual financial statements that detail its income, expenses, and remittances to the Treasury.

Federal Reserve Bulletin: The Federal Reserve also includes information about remittances in its periodic bulletins and reports to Congress.

Have a great weekend! Take time to pray for peace!

May we have peace beyond all understanding 🙏